Etex resists to a challenging market context and delivers strong and improving 2023 results, preparing for further growth

Highlights

• For another year in a row Etex achieved new record operational performance, especially in revenue and REBITDA, while accelerating on its sustainability ambitions.

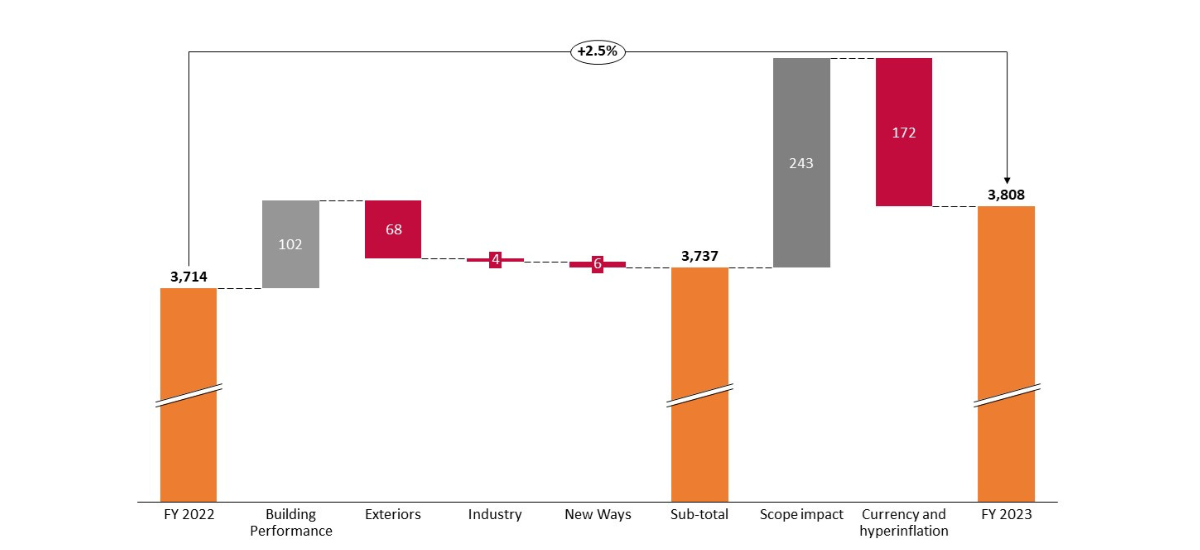

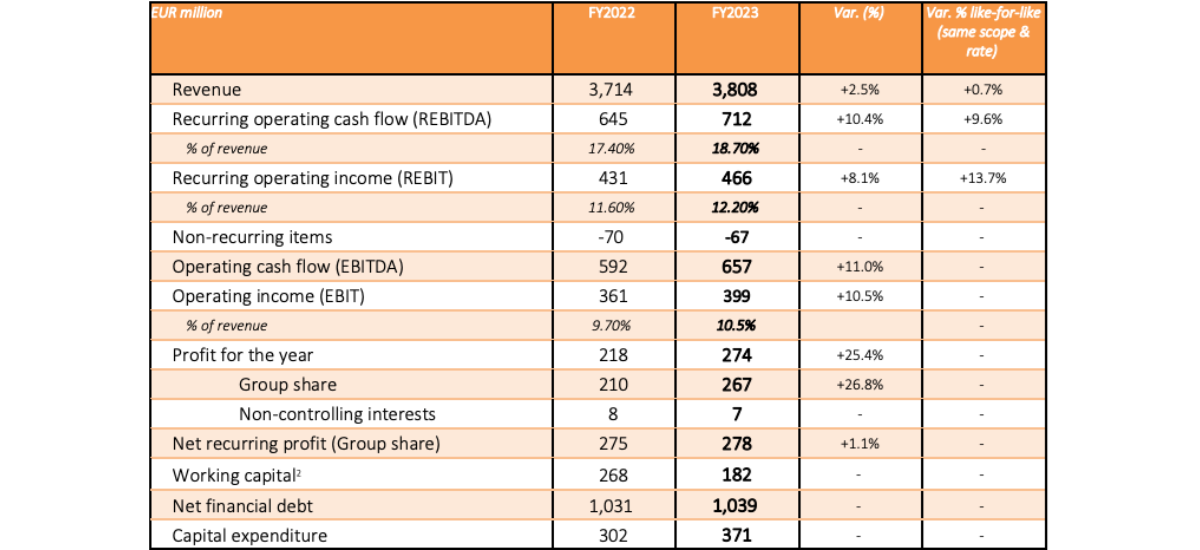

• Record revenue of EUR 3.808 billion, despite low market demand, corresponding to an increase of 2.5% compared to 2022. This is attributable mainly to growth in plasterboard solutions and to additional revenue from the new Insulation division. Like-for-like¹ it represents an increase of 0.7%.

• Highest value ever for REBITDA, at EUR 712 million, a 10.4% increase versus 2022, driven mostly by responsive margin management. Like-for-like¹ increase of 9.6% versus 2022.

• Increase of the net profit (Group share) to EUR 267 million, a 26.8% improvement compared to 2022, thanks to the one-off gain on reselling an interest rates’ hedging contract. The net recurring profit (Group share) also improved, at EUR 278 million, +1.1% year-on-year. The net recurring profit was negatively impacted by hyperinflation accounting in Argentina for EUR 23 million.

• Almost unchanged net financial debt at EUR 1.039 billion versus EUR 1.031 billion in 2022. Strong cash flow generation and proceeds from disposal of some assets and businesses allowed to finance record high capital expenditure investments in infrastructure (EUR 371 million), and the acquisitions of Skamol (high-temperature insulation), Superglass (glass wool insulation) and SCALAMID (fibre cement).

• Etex stopped all operations in Russia.

• Gross dividend: proposal by the Board of Directors of EUR 1.03 per share (+10.8%).

• Sustainability: significant progress towards Etex’s 2030 sustainability ambitions on decarbonisation, circularity, customer engagement, and diversity, equity and inclusion.

• Outlook for 2024: amidst ongoing uncertainty and market volatility across geographies expected to persist, with current soft and volatile volumes and no imminent full recovery in sight, Etex targets for a continuing strong REBITDA margin. Etex will continue investing in 2024, preparing for further growth and keep exploring potential strategic opportunities.

• Etex emphasises that, with its product portfolio, it is part of the solution to reach the ambitious EU environmental targets. In view of this urgent challenge, the company calls for a holistic, and effective plan to boost, finance and simplify access to new build and renovation, in each of the EU countries.

• Etex’s combined Annual and Sustainability Report 2023 will be published on 23 April 2024.

• Watch Etex’s CEO Bernard Delvaux short video on the full-year results.

Comments from Bernard Delvaux, CEO of Etex: “Even more so than 2022, 2023 was a challenging year marked by volatility, uncertainty, and severe drops in demand across the world as we observed the continued impacts of increased energy prices and interest rates. Combined with tougher financing possibilities by banks, all these circumstances meant that both renovation and new construction levels dropped globally. Devaluation of some foreign currencies and hyperinflation accounting also had significant effects on our results. Despite all these challenges, I am extremely proud to share that Etex navigated these difficult waters very well and delivered yet again another record year. This includes our highest ever revenue and REBITDA, among others.

This strong performance stems from our anticipation in making strategic decisions and changes at global, regional, and local levels, ensuring continued proximity with our customers. This is also a result of even tighter cost monitoring in 2023 without ever losing sight of our long-term ambitions and continuing to improve our strong industrial footprint. Our factories are at the heart of what we do. With a record EUR 371 million capital expenditure, we further invested to maintain and improve our production facilities.

We continued to advance on our strategic position as a world leader in lightweight construction through several key acquisitions within our core expertise, namely Skamol in high-temperature insulation, Superglass in glass wool insulation, SCALAMID in fibre cement and most recently in February 2024 BGC’s plasterboard and fibre cement businesses. In the summer, we also completed the process of exiting Russia by divesting two operating sites in the country. These sites were part of the original URSA insulation footprint acquired before the invasion took place. We are actively preparing to help rebuild Ukraine as soon as it is possible and safe to do so.

2023 was also a year of acceleration on our 2030 sustainability ambitions. To name a few, we achieved a 22.8% CO₂ absolute emission reduction in scopes 1 and 2 compared to our 2018 reference baseline. We also had over 7.4% recycled material across product technologies, surpassing our 2022 performance by 26%. Etex stands out as a top recycling performer in Europe with 8.6% recycled gypsum, close to 47% recycled polystyrene and around 75% recycled glass. Finally, we remain in the top 10% of construction products companies worldwide in terms of ESG risk rating.

For 2024, we expect market conditions to remain uncertain and unstable across our geographies, with soft and volatile volumes and no full recovery, even if interest rates could stabilise. More than ever, we will remain responsive on a month-per-month, country-by-country and product-by-product basis to navigate this unpredictability. On the other hand, we are confident in the mid- to long-term perspectives of Etex and the intrinsic sustainable value of our products and solutions to answer the needs in renovation and new construction for our customers. This is why we will remain on the lookout in 2024 for new strategic opportunities and will continue to invest and prepare for further growth. Overall, we expect continued strong REBITDA margin in 2024.

As a final thought, we want to emphasise that industry players of sustainable construction like Etex are part of the solution to meet the goals set in the Paris Agreement on climate change through buildings that must become energy efficient. Looking at for example the European Union, more than 40% of the energy consumed is used in buildings and more than 30% of energy-related greenhouse gasses emissions come from buildings. Next to new building activities, and according to current high energy standards, renovating old building stock should hence be a top priority. With our portfolio of building materials such as glass wool and extruded polystyrene insulation, plasterboard, fibre cement boards and fire protection materials, Etex has the solutions to reach the ambitious targets. But in view of the huge challenge, a holistic and effective plan to boost renovation is needed, to finance and simplify the renovation process, in each of the EU countries."

Outstanding performance despite volatility and uncertainty

In 2023, Etex recorded a revenue of EUR 3.808 billion for a year-on-year revenue increase of 2.5% when including the impact of scope changes, translation, and hyperinflation. Like-for-like¹ (same currency exchange rates and scope) this represents a revenue increase of 0.7%. This performance is mostly attributable to price management and the ability to cover purchasing and payroll cost increases despite soft and volatile volumes overall. The 6.9% net positive scope impact compared with 2022 is attributable to additional revenues from recent acquisitions, namely Skamol and Superglass in 2023, as well as URSA in 2022.

The recurring operating cash flow (REBITDA) reached EUR 712 million, its highest absolute value ever, for a 10.4% increase. This performance is mainly attributable to increased revenues and limited cost increases, jointly with the positive impact of the acquisition of European insulation leader URSA, as well as Skamol and Superglass. This represents a like-for-like¹ increase of 9.6% compared to 2022. The REBITDA also reached an improved 18.7% in terms of percentage of sales, compared to 17.4% in 2022.

The net profit (Group share) increased to EUR 267 million, a 26.8% improvement compared to 2022, thanks to the one-off gain on reselling of an interest rates hedging contract. The net recurring profit (Group share) also improved, at EUR 278 million, +1.1% year-on-year.

Next to record REBITDA performance, Etex achieved a further reduction of working capital in 2023 by continuous anticipation of inventories and production planning and focus on trade debtors and creditors management. This combination allowed sufficient generation of cash over the year to compensate for Etex’s highest capital expenditure ever (EUR 371 million, versus EUR 302 million in 2022) and to cover the new business acquisitions.

By end 2023, Etex’s net financial debt was at EUR 1.039 billion, compared to EUR 1.031 billion for 2022.

At the Shareholders’ Meeting on 22 May 2024, the Board of Directors of Etex will propose a gross dividend increase of 10.8% to EUR 1.03 per share.

Revenue by geography and division, greatly impacted by hyperinflation accounting and currency devaluations

2023 was a challenging year marked by volatility, uncertainty and severe drops in demand across the world as Etex observed the continued impacts of increased energy prices and interest rates. Combined with tougher financing possibilities by banks, all these circumstances meant that both renovation and new construction levels dropped globally. Devaluation of foreign currencies, in particular in Nigeria, coupled with hyperinflation accounting for Argentina, also had very significant effects on Etex’s results.

The Building Performance division, specialising in plasterboard, fibre cement boards and fire protection materials for technical construction, registered a like-for-like¹ revenue increase of 4.2% to reach EUR 2.381 billion. Despite significant volume drops overall, Etex’s largest division limited negative impacts through clever optimisations and good price management to ensure strong profitability.

The Exteriors division, which focuses on fibre cement exterior solutions, saw a like-for-like¹ revenue decrease of 10.1% at EUR 595 million. This is mainly attributable to decreases in volumes compared to 2022 given drops in residential housing in Europe driven by cost of construction and increasing interest rates. A slowdown in Europe was partially offset by the beginnings of a market recovery in Latin America and Asia-Pacific.

The revenue of Etex’s Industry division, centred around fire protection and high-performance insulation, was down by 2.0% like-for-like¹, amounting to EUR 244 million and positively evolving compared to 2022 thanks to the acquisition of Skamol which contributed for EUR 47 million to this figure through seven months of activity. Strong pressure was felt on volumes, mainly in the segments linked to the heavy industry and construction sectors such as the fire-rated assemblies in Europe. Steady price management allowed the division to limit the volume impact on top-line. The energy segment shows a mixed picture in 2023 with a conjunctural decrease of project in oil and gas in Asia-Pacific, the Middle East and Africa compensated by strong investment in green energy investments in Europe, with this trend expected to continue through 2024.

The sales of the Insulation division, specialised in glass mineral wool and extruded polystyrene (XPS), was up by EUR 214 million due to the timing of acquisition in 2022 and recorded a revenue of EUR 526 million. In 2023, the volume drops resulted from reduced demand globally. A construction sector being plagued by a high interest rate environment, heavy drops in new build, and postponement was the norm. Insulation was amongst the first to see this drastically changed landscape. However, Insulation was able to protect its market shares and continue to focus on performance management. As the middle and long-term market foundations are solid and growth will come back, the division is preparing plans for added capacity in glass mineral wool to keep the current market share and grow with the market.

The revenue of the New Ways division, based on high-tech offsite solutions, was down by 9.8% like-for-like¹, to EUR 62 million. The division delivered results short of its top line target due to construction delays in a complicated environment and termination of the e-Loft activity. It successfully launched its new brand Remagin, which brings together the highly qualified teams of former brands Sigmat, EOS and Horizon while still benefitting from the expertise of Evolusion Innovation, Etex’s offsite design and engineering consultancy company.

Key developments

On the mergers, acquisitions, and divestments side, 2023 saw important developments:

• In early May, Etex completed the acquisition of Skamol, a leading Danish manufacturer of fire protection and specialty insulation materials with sites in Denmark and Poland. This acquisition further consolidates Etex’s portfolio of sustainable solutions in a market that is strongly supported by the need for energy efficient insulation products and solutions.

• In late June, Etex acquired Superglass, a top three player in the United Kingdom and Ireland in the growing glass mineral wool insulation market. Through this deal, Etex expands its already strong activities in the UK and complements the extensive European sales and production network of its Insulation division where it is already active with URSA.

• In August, Etex completed its exit from Russia by divesting its two operating sites in the country. These sites were part of the original URSA footprint acquired before the invasion took place. Etex is also actively preparing to help rebuild Ukraine as soon as it is possible and safe to do so.

• In late December, Etex took a significant step to further enhance architectural design with the acquisition of SCALAMID, a Polish manufacturer of fibre cement panels featuring cutting-edge digital printing and coating technology. This strategic move offers new possibilities for customers’ design and reinforces Etex's commitment to advancing innovation in the lightweight construction industry.

• Moreover, as latest acquisition, in February 2024, Etex closed the acquisition of Australian construction materials company BGC’s plasterboard and fibre cement businesses. Through this deal, Etex expands its sustainable activities in the attractive Australian and New Zealand markets, with significant growth opportunities.

Today, the Etex strategy is summarised in its strategic framework, a global compass that guides the company’s future plans and shapes its decision-making and investments. This framework focuses on the five platforms of Etex: Gypsum, Fibre cement, Passive fire protection and High-performance insulation, Insulation, and Systems and Solutions. All these platforms are supported by four business drivers: Sustainability and Innovation, Engaged people, Operational excellence, and Customer engagement.

Etex’s achievements in 2023 related to its “Sustainability and Innovation” driver demonstrate that the company is making significant progress towards its 2030 sustainability ambitions. Highlights include:

• Decarbonisation: 22.8% CO₂ absolute emission reduction in scopes 1 and 2 compared to Etex’s 2018 reference baseline, making considerable progress towards its 2030 goal of -35% CO₂ (scopes 1 and 2) intensity reduction.

As illustration, Etex acquired Skamol in May and immediately decided to invest for a low carbon future in its calcium silicate plant in Branden, Denmark. This plant is cutting its absolute emissions by 43% compared to 2022, a significant reduction in carbon footprint through major electrification of part of the plant, using green energy and innovative technology - a total investment of EUR 9 million.

• Circularity (recycling): Etex achieved over 7.4% recycled material across product technologies, surpassing its 2022 performance by 26%. The company stands out as the top performer in Europe with 8.6% recycled gypsum, close to 47% recycled polystyrene and around 75% recycled glass.

• Circularity (waste to landfill): Etex further reduced waste sent from its factories to landfill. The company decreased waste in absolute values by 5% in 2023 (a 16% reduction on unchanged scope), and 28% since 2018 (a 30% reduction on unchanged scope).

Circularity can be exemplified with Etex’s take-back offers for which Etex is a leader in Europe. In Italy, the ‘PregyGreenService’ provided by the brand Siniat helped installers and contractors to easily dispose of 20,000 tons of plasterboard waste in 2023, addressing compliance challenges and environmental criteria. This service includes pick-up, transportation, and recycling, with additional support for retailers in waste collection management.

Circularity is also demonstrated through packaging. Etex’s brand Promat managed to significantly reduce the use of plastic packaging. At its passive fire protection plant in Dubai, United Arab Emirates, Etex eliminated 84% of plastic by replacing plastic bags containing its cementitious sprays with recycled paper packaging. And in the microporous plant in Sint-Niklaas, Belgium, Etex eliminated 78% of plastic by replacing plastic packaging with recycled cardboard and paper packaging.

• Customer engagement: Etex secured 70% coverage of its European turnover with independently verified Environmental Product Declarations (EPDs) across divisions, up from 58% in 2022. This advancement aligns with the elevated expectations of Etex’s customers who request meeting technical requirements associated with transparent environmental considerations.

• Diversity, equity and inclusion (DE&I): Etex unveiled its diversity, equity and inclusion commitment and policy in 2023 and built a global DE&I ambassador community with 110 volunteers from 26 countries. Likewise, the company educated more than 4,600 office-based teammates on unconscious bias.

Next to these results, Etex maintained a worldwide top 10% ESG Sustainalytics rating in the construction products category, ranking 11th out of 150 companies with a final score of 17.9. For the second consecutive year, Etex also achieved an EcoVadis SILVER rating underscoring the company’s collective dedication to sustainability and ethical practices.

When it comes to its “Engaged people” priority, Etex is proud to have warmly welcomed and onboarded more than 700 new teammates following the acquisitions of four new companies. Talent acquisition was a highlight in 2023, with Etex creating its own recruitment capabilities to identify the right talent that will thrive in the organisation and to improve the candidate experience throughout the process. Etex continued to foster a culture of recognition through the Etex Awards, including its CEO Award for a game-changing contribution. The latter was won in 2023 by the Export Team of the Exteriors division comprised of 25 teammates across Belgium, Malaysia, France, Italy, and Chile. In total, 3219 awards were given to recognise teammates over the year.

Etex’s “Operational excellence” focus in 2023 required, just like in 2022, a constant anticipation and adaptation to extreme uncertainties. Through the agility of its plants to demand volatility Etex was able to deliver to its customers. The company prepared for the future by investing a record EUR 371 million (a 23% increase versus last year with an amount of EUR 302 million) in capital expenditure projects to maintain factories, increase production capacity and make plants safer and more sustainable. This includes the launch of new production lines in Nigeria and Italy, continued works in the United Kingdom (Bristol) where Etex is finalising its largest plasterboard plant ever, and an investment for a plasterboard site in Romania. Etex factories’ waste reduction and cost improvement measures implemented in 2023 also delivered over EUR 50 million while the stretch target of energy consumption reduction of 5% was reached by several plants. In terms of safety, Etex decreased its total accident frequency rate to 2.96. This is an improvement by 21% compared to 2022. The company also increased on its main leading indicator, safety intensity, by 7% to 1.80. However, Etex cannot be satisfied with its safety performance overall following two casualties over the year, one with an Etex teammate in Argentina and one with a contractor in Spain. In 2024, Etex will put even more focus on serious incident and fatality prevention and on safety processes to improve towards its ambition of zero accident.

For its “Customer engagement” driver, and following a strong focus on customer journeys, the company also recorded improved Net Promoter Scores (NPS) - measuring customer loyalty, satisfaction, and enthusiasm - in many key countries despite a challenging situation. Etex saw further impact of the platforms launched in 2022, next to the divisions. These are forward-looking growth platforms, allowing the company to focus on mid- and long-term growth opportunities for each of the five technologies such as gypsum and fibre cement. Etex also strengthened the roles of divisions and local leadership teams who are in direct line to serve its customers and deliver day-to-day. In 2023, Etex initiated quarterly strategic discussions with each platform. From these, teams derive inspiration to improve the customer journey in local markets. This will be continued in 2024 as customer satisfaction is one of the main topics under regular review. Finally, Etex also launched its new version of SAP S/4HANA, an advanced enterprise resource planning and integration platform of data from finance, accounting, controlling, procurement, sales, manufacturing, plant maintenance, project system, and product lifecycle management.

Outlook for FY 2024

For 2024, Etex expects the market conditions to remain uncertain and unstable, with soft and volatile volumes and no full recovery even if interest rates could stabilise or decrease in some countries. More than ever, the company will remain responsive on a month-per-month, country-by-country and product-by-product basis to navigate this uncertainty. Overall, Etex continues to expect continued strong REBITDA margin in 2024. The company is confident in its mid- to long-term perspectives given the intrinsic sustainable value of its products and solutions to answer the needs in renovation and new construction for customers. This is why Etex will remain on the lookout in 2024 for new strategic opportunities and will continue to invest and prepare for further growth.

Changes to the Board of Directors

Mr. T. Scalmani left the Board of Directors on 6 April 2023. The mandates of JoVB BV, represented by Mr. J. Van Biesbroeck; ARGALI CAPITAL BV, represented by Mr. P. Emsens; CT IMPACT BV, represented by Mrs. C. Thijssen; Mr. C. Simonard; Tee&Tee BV, represented by Mr. T. Vanlancker; and GUVO BV, represented by Mr. G. Voortman will expire at the next general shareholders’ meeting on 22 May 2024 and will be renewed or replaced. Further details will be made available in the convening notice to the general shareholders’ meeting.

Key figures for FY 2023

¹ The like-for-like percentages compare FY 2023 to FY 2022, the latter being converted with identical exchange rates, while excluding the impact of hyperinflation, of the newly acquired businesses, Skamol, Superglass (2023) URSA (2022) and of the discontinued New Ways business in France (e-Loft); the impacts of the Ukrainian and Russian businesses being also neutralised.

² Values are expressed excluding the favourable impact of the non-recourse factoring programme (EUR 243 million as of 31/12/2023 vs EUR 259 million for the prior year).

The consolidated financial statements for the year 2023 will be approved by the Board of Directors on 18 April 2024 and will be presented for approval at the Shareholders’ Meeting.

The statutory auditor, PwC Bedrijfsrevisoren bv, represented by Peter Van den Eynde has confirmed that the audit, which is substantially complete, has not to date revealed any material misstatement in the draft consolidated statement of financial position, consolidated income statement and consolidated statement of comprehensive income, and that the accounting data reported in the press release is consistent, in all material respects, with the draft consolidated statement of financial position, consolidated income statement and consolidated statement of comprehensive income, from which it has been derived.

The Consolidated income statement, Consolidated statement of comprehensive income and Consolidated statement of financial position can be found in annex on pages 12 and 13.

The 2023 Annual Report of the company will be available on Etex’s website as of 23 April 2024.